India to witness GDP growth of 6.0 per cent to 6.8 per cent in 2023-24, depending on the trajectory of economic and political developments globally.

The optimistic growth forecasts stem from a number of positives like the rebound of private consumption given a boost to production activity, higher Capital Expenditure (Capex), near-universal vaccination coverage enabling people to spend on contact-based services, such as restaurants, hotels, shopping malls, and cinemas, as well as the return of migrant workers to cities to work in construction sites leading to a significant decline in housing market inventory, the strengthening of the balance sheets of the Corporates, a well-capitalised public sector banks ready to increase the credit supply and the credit growth to the Micro, Small, and Medium Enterprises (MSME) sector to name the major ones.

The Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman tabled the Economic Survey 2022-23 in Parliament today, which projects a baseline GDP growth of 6.5 per cent in real terms in FY24. The projection is broadly comparable to the estimates provided by multilateral agencies such as the World Bank, the IMF, and the ADB and by RBI, domestically.

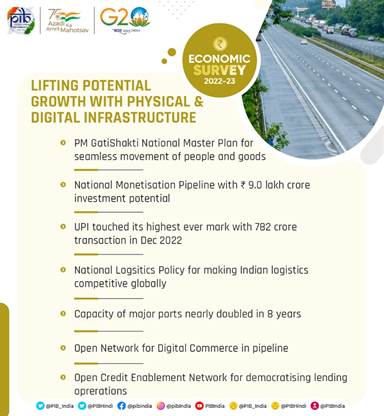

It says, growth is expected to be brisk in FY24 as a vigorous credit disbursal, and capital investment cycle is expected to unfold in India with the strengthening of the balance sheets of the corporate and banking sectors. Further support to economic growth will come from the expansion of public digital platforms and path-breaking measures such as PM GatiShakti, the National Logistics Policy, and the Production-Linked Incentive schemes to boost manufacturing output.

The Survey says, in real terms, the economy is expected to grow at 7 per cent for the year ending March 2023. This follows an 8.7 per cent growth in the previous financial year.

Despite the three shocks of COVID-19, Russian-Ukraine conflict and the Central Banks across economies led by Federal Reserve responding with synchronised policy rate hikes to curb inflation, leading to appreciation of US Dollar and the widening of the Current Account Deficits (CAD) in net importing economies, agencies worldwide continue to project India as the fastest-growing major economy at 6.5-7.0 per cent in FY23.

According to Survey, India’s economic growth in FY23 has been principally led by private consumption and capital formation and they have helped generate employment as seen in the declining urban unemployment rate and in the faster net registration in Employee Provident Fund. Moreover, World’s second-largest vaccination drive involving more than 2 billion doses also served to lift consumer sentiments that may prolong the rebound in consumption. Still, private capex soon needs to take up the leadership role to put job creation on a fast track.

It also points out that the upside to India’s growth outlook arises from (i) limited health and economic fallout for the rest of the world from the current surge in Covid-19 infections in China and, therefore, continued normalisation of supply chains; (ii) inflationary impulses from the reopening of China’s economy turning out to be neither significant nor persistent; (iii) recessionary tendencies in major Advanced Economies (AEs) triggering a cessation of monetary tightening and a return of capital flows to India amidst a stable domestic inflation rate below 6 per cent; and (iv) this leading to an improvement in animal spirits and providing further impetus to private sector investment.

The Survey says, the credit growth to the Micro, Small, and Medium Enterprises (MSME) sector has been remarkably high, over 30.6 per cent, on average during Jan-Nov 2022, supported by the extended Emergency Credit Linked Guarantee Scheme (ECLGS) of the Union government. It adds that the recovery of MSMEs is proceeding apace, as is evident in the amounts of Goods and Services Tax (GST) they pay, while the Emergency Credit Linked Guarantee Scheme (ECGLS) is easing their debt servicing concerns.

Apart from this, increase in the overall bank credit has also been influenced by the shift in borrower’s funding choices from volatile bond markets, where yields have increased, and external commercial borrowings, where interest and hedging costs have increased, towards banks. If inflation declines in FY24 and if real cost of credit does not rise, then credit growth is likely to be brisk in FY24.

The Capital Expenditure (Capex) of the central government, which increased by 63.4 per cent in the first eight months of FY23, was another growth driver of the Indian economy in the current year, crowding in the private Capex since the January-March quarter of 2022. On current trend, it appears that the full year’s capital expenditure budget will be met. A sustained increase in private Capex is also imminent with the strengthening of the balance sheets of the Corporates and the consequent increase in credit financing it has been able to generate.

Dwelling on halt in construction activities during the Pandemic, the Survey underscores that vaccinations have facilitated the return of migrant workers to cities to work in construction sites as the rebound in consumption spilled over into the housing market. This is evident in the housing market witnessing a significant decline in inventory overhang to 33 months in Q3 of FY23 from 42 months last year.

It also says that the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) has been directly providing jobs in rural areas and indirectly creating opportunities for rural households to diversify their sources of income generation. Schemes like PM-Kisan and PM Garib Kalyan Yojana have helped in ensuring food security in the country, and their impact was also endorsed by the United Nations Development Programme (UNDP). The results of the National Family Health Survey (NFHS) also show improvement in rural welfare indicators from FY16 to FY20, covering aspects like gender, fertility rate, household amenities, and women empowerment.

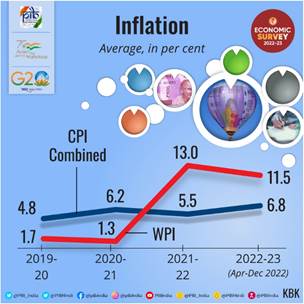

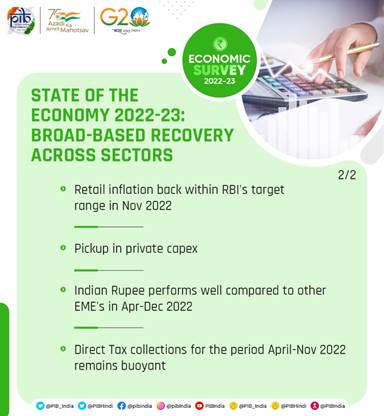

The Survey notes with optimism that Indian economy appears to have moved on after its encounter with the pandemic, staging a full recovery in FY22 ahead of many nations and positioning itself to ascend to the pre-pandemic growth path in FY23. Yet in the current year, India has also faced the challenge of reining in inflation that the European strife accentuated. Measures taken by the government and RBI, along with the easing of global commodity prices, have finally managed to bring retail inflation below the RBI upper tolerance target in November 2022.

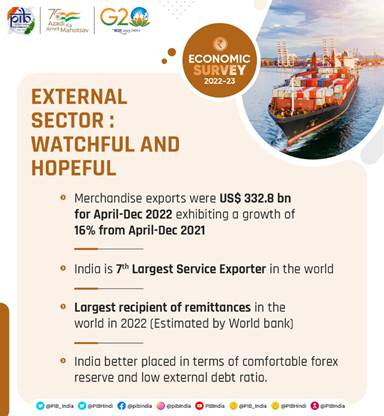

It, however, cautions that the challenge of the depreciating rupee, although better performing than most other currencies, persists with the likelihood of further increases in policy rates by the US Fed. The widening of the CAD may also continue as global commodity prices remain elevated and the growth momentum of the Indian economy remains strong. The loss of export stimulus is further possible as the slowing world growth and trade shrinks the global market size in the second half of the current year.

Therefore, the Global growth has been projected to decline in 2023 and is expected to remain generally subdued in the following years as well. The slowing demand will likely push down global commodity prices and improve India’s CAD in FY24. However, a downside risk to the Current Account Balance stems from a swift recovery driven mainly by domestic demand, and to a lesser extent, by exports. It also adds that the CAD needs to be closely monitored as the growth momentum of the current year spills over into the next.

The Survey brings to the fore an interesting fact that in general, global economic shocks in the past were severe but spaced out in time, but this changed in the third decade of this millennium, as at least three shocks have hit the global economy since 2020.

It all started with the pandemic-induced contraction of the global output, followed by the Russian-Ukraine conflict leading to a worldwide surge in inflation. Then, the central banks across economies led by the Federal Reserve responded with synchronised policy rate hikes to curb inflation. The rate hike by the US Fed drove capital into the US markets causing the US Dollar to appreciate against most currencies. This led to the widening of the Current Account Deficits (CAD) and increased inflationary pressures in net importing economies.

The rate hike and persistent inflation also led to a lowering of the global growth forecasts for 2022 and 2023 by the IMF in its October 2022 update of the World Economic Outlook. The frailties of the Chinese economy further contributed to weakening the growth forecasts. Slowing global growth apart from monetary tightening may also lead to a financial contagion emanating from the advanced economies where the debt of the non-financial sector has risen the most since the global financial crisis. With inflation persisting in the advanced economies and the central banks hinting at further rate hikes, downside risks to the global economic outlook appear elevated.

India’s Economic Resilience and Growth Drivers

The Survey points out that factors like monetary tightening by the RBI, the widening of the CAD, and the plateauing growth of exports have essentially been the outcome of geopolitical strife in Europe. As these developments posed downside risks to the growth of the Indian economy in FY23, many agencies worldwide have been revising their growth forecast of the Indian economy downwards. These forecasts, including the advance estimates released by the NSO, now broadly lie in the range of 6.5-7.0 per cent.

Despite the downward revision, the growth estimate for FY23 is higher than for almost all major economies and even slightly above the average growth of the Indian economy in the decade leading up to the pandemic.

IMF estimates India to be one of the top two fast-growing significant economies in 2022. Despite strong global headwinds and tighter domestic monetary policy, if India is still expected to grow between 6.5 and 7.0 per cent, and that too without the advantage of a base effect, it is a reflection of India’s underlying economic resilience; of its ability to recoup, renew and re-energise the growth drivers of the economy. India’s economic resilience can be seen in the domestic stimulus to growth seamlessly replacing the external stimuli. The growth of exports may have moderated in the second half of FY23. However, their surge in FY22 and the first half of FY23 induced a shift in the gears of the production processes from mild acceleration to cruise mode.

Manufacturing and investment activities consequently gained traction. By the time the growth of exports moderated, the rebound in domestic consumption had sufficiently matured to take forward the growth of India’s economy. Private Consumption as a percentage of GDP stood at 58.4 per cent in Q2 of FY23, the highest among the second quarters of all the years since 2013-14, supported by a rebound in contact-intensive services such as trade, hotel and transport, which registered sequential growth of 16 per cent in real terms in Q2 of FY23 compared to the previous quarter.

Although domestic consumption rebounded in many economies, the rebound in India was impressive for its scale. It contributed to a rise in domestic capacity utilisation. Domestic private consumption remains buoyant in November 2022. Moreover, RBI’s most recent survey of consumer confidence released in December 2022 pointed to improving sentiment with respect to current and prospective employment and income conditions.

The Survey also points to another recovery and adds that the “release of pent-up demand” was reflected in the housing market too as demand for housing loans picked up. Consequently, housing inventories have declined, prices are firming up, and construction of new dwellings is picking up pace and this has stimulated innumerable backward and forward linkages that the construction sector is known to carry. The universalisation of vaccination coverage also has a significant role in lifting the housing market as, in its absence, the migrant workforce could not have returned to construct new dwellings.

Apart from housing, construction activity, in general, has significantly risen in FY23 as the much-enlarged capital budget (Capex) of the central government and its public sector enterprises is rapidly being deployed.

Going by the Capex multiplier estimated for the country, the economic output of the country is set to increase by at least four times the amount of Capex. States, in aggregate, are also performing well with their Capex plans. Like the central government, states also have a larger capital budget supported by the centre’s grant-in-aid for capital works and an interest-free loan repayable over 50 years.

Also, a capex thrust in the last two budgets of the Government of India was not an isolated initiative meant only to address the infrastructure gaps in the country. It was part of a strategic package aimed at crowding-in private investment into an economic landscape broadened by the vacation of non-strategic PSEs (disinvestment) and idling public sector assets.

Here, three developments support this firstly the significant increase in the Capex budget in FY23, as well as its high rate of spending, secondly direct tax revenue collections have been highly buoyant, and so have GST collections, which should ensure the full expending of the Capex budget within the budgeted fiscal deficit. The growth in revenue expenditure has also been limited to pave the way for higher growth in Capex and thirdly the pick-up in private sector investment since the January-March quarter of 2022. Evidence shows an increasing trend in announced projects and capex spending by the private players.

While an increase in export demand, rebound in consumption, and public capex have contributed to a recovery in the investment/manufacturing activities of the corporates, their stronger balance sheets have also played a big part equal measure to realising their spending plans. As per the data on non-financial debt from the Bank for International Settlements, in the course of the last decade, Indian non-financial private sector debt and non-financial corporate debt as a share of GDP declined by nearly thirty percentage points.

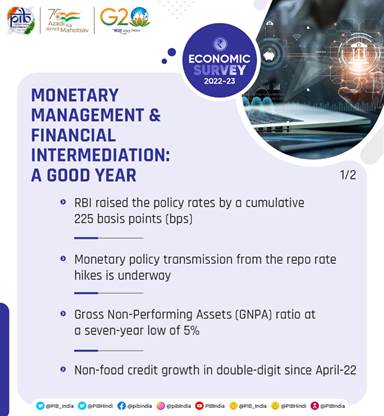

The banking sector in India has also responded in equal measure to the demand for credit as the Year-on-Year growth in credit since the January-March quarter of 2022 has moved into double-digits and is rising across most sectors.

The finances of the public sector banks have seen a significant turnaround, with profits being booked at regular intervals and their Non-Performing Assets (NPAs) being fast-tracked for quicker resolution/liquidation by the Insolvency and Bankruptcy Board of India (IBBI). At the same time, the government has been providing adequate budgetary support for keeping the PSBs well-capitalized, ensuring that their Capital Risk-Weighted Adjusted Ratio (CRAR) remains comfortably above the threshold levels of adequacy. Nonetheless, financial strength has helped banks make up for lower debt financing provided by corporate bonds and External Commercial Borrowings (ECBs) so far in FY23. Rising yields on corporate bonds and higher interest/hedging costs on ECBs have made these instruments less attractive than the previous year.

RBI has projected headline inflation at 6.8 per cent in FY23, which is outside its target range. At the same time, it is not high enough to deter private consumption and also not so low as to weaken the inducement to invest.

Macroeconomic and Growth Challenges in the Indian Economy

After the impact of the two waves of the pandemic seen in a significant GDP contraction in FY21, the quick recovery from the virus in third wave of Omicron contributed to minimising the loss of economic output in the January-March quarter of 2022. Consequently, output in FY22 went past its pre-pandemic level in FY20, with the Indian economy staging a full recovery ahead of many nations. However, the conflict in Europe necessitated a revision in expectations for economic growth and inflation in FY23. The country’s retail inflation had crept above the RBI’s tolerance range in January 2022 and it remained above the target range for ten months before returning to below the upper end of the target range of 6 per cent in November 2022.

It says that the Global commodity prices may have eased but are still higher compared to pre-conflict levels and they have further widened the CAD, already enlarged by India’s growth momentum. For FY23, India has sufficient forex reserves to finance the CAD and intervene in the forex market to manage volatility in the Indian rupee.

Outlook: 2023-24

Dwelling on the Outlook for 2023-24, the Survey says, India’s recovery from the pandemic was relatively quick, and growth in the upcoming year will be supported by solid domestic demand and a pickup in capital investment. It says that aided by healthy financials, incipient signs of a new private sector capital formation cycle are visible and more importantly, compensating for the private sector’s caution in capital expenditure, the government raised capital expenditure substantially.

Budgeted capital expenditure rose 2.7 times in the last seven years, from FY16 to FY23, re-invigorating the Capex cycle. Structural reforms such as the introduction of the Goods and Services Tax and the Insolvency and Bankruptcy Code enhanced the efficiency and transparency of the economy and ensured financial discipline and better compliance, the Survey added.

Global growth is forecasted to slow from 3.2 per cent in 2022 to 2.7 per cent in 2023 as per IMF’s World Economic Outlook, October 2022. A slower growth in economic output coupled with increased uncertainty will dampen trade growth. This is seen in the lower forecast for growth in global trade by the World Trade Organisation, from 3.5 per cent in 2022 to 1.0 per cent in 2023.

On the external front, risks to the current account balance stem from multiple sources. While commodity prices have retreated from record highs, they are still above pre-conflict levels. Strong domestic demand amidst high commodity prices will raise India’s total import bill and contribute to unfavourable developments in the current account balance. These may be exacerbated by plateauing export growth on account of slackening global demand. Should the current account deficit widen further, the currency may come under depreciation pressure.

Entrenched inflation may prolong the tightening cycle, and therefore, borrowing costs may stay ‘higher for longer’. In such a scenario, global economy may be characterised by low growth in FY24. However, the scenario of subdued global growth presents two silver linings – oil prices will stay low, and India’s CAD will be better than currently projected. The overall external situation will remain manageable.

India’s Inclusive Growth

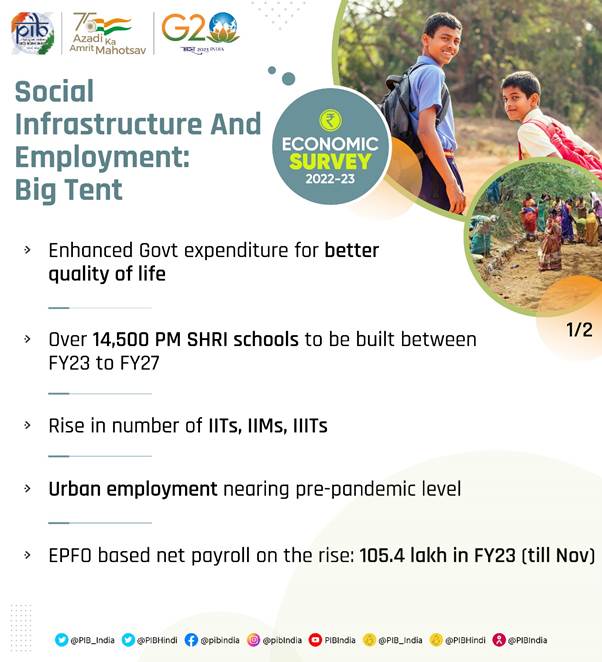

The Survey emphasises that growth is inclusive when it creates jobs. Both official and unofficial sources confirm that employment levels have risen in the current financial year, as the Periodic Labour Force Survey (PLFS) shows that the urban unemployment rate for people aged 15 years and above declined from 9.8 per cent in the quarter ending September 2021 to 7.2 per cent one year later (quarter ending September 2022). This is accompanied by an improvement in the labour force participation rate (LFPR) as well, confirming the emergence of the economy out of the pandemic-induced slowdown early in FY23.

In FY21, the Government announced the Emergency Credit Line Guarantee Scheme, which succeeded in shielding micro, small and medium enterprises from financial distress. A recent CIBIL report (ECLGS Insights, August 2022) showed that the scheme has supported MSMEs in facing the COVID shock, with 83 per cent of the borrowers that availed of the ECLGS being micro-enterprises. Among these micro units, more than half had an overall exposure of less than Rs10 lakh.

Furthermore, the CIBIL data also shows that ECLGS borrowers had lower non-performing asset rates than enterprises that were eligible for ECLGS but did not avail of it. Further, the GST paid by MSMEs after declining in FY21 has been rising since and now has crossed the pre-pandemic level of FY20, reflecting the financial resilience of small businesses and the effectiveness of the pre-emptive government intervention targeted towards MSMEs.

Moreover, the scheme implemented by the government under the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) has been rapidly creating more assets in respect of “Works on individual’s land” than in any other category. In addition, schemes like PM-KISAN, which benefits households covering half the rural population, and PM Garib Kalyan Anna Yojana have significantly contributed to lessening impoverishment in the country.

The UNDP Report of July 2022 stated that the recent inflationary episode in India would have a low poverty impact due to well-targeted support. In addition, the National Family Health Survey (NFHS) in India shows improved rural welfare indicators from FY16 to FY20, covering aspects like gender, fertility rate, household amenities, and women empowerment.

So far, India has reinforced the country’s belief in its economic resilience as it has withstood the challenge of mitigating external imbalances caused by the Russian-Ukraine conflict without losing growth momentum in the process. India’s stock markets had a positive return in CY22, unfazed by withdrawals by foreign portfolio investors. India’s inflation rate did not creep too far above its tolerance range compared to several advanced nations and regions.

India is the third-largest economy in the world in PPP terms and the fifth-largest in market exchange rates. As expected of a nation of this size, the Indian economy in FY23 has nearly “recouped” what was lost, “renewed” what had paused, and “re-energised” what had slowed during the pandemic and since the conflict in Europe.

The global economy battles through a unique set of challenges

The Survey narrates about six challenges faced by the Global Economy. The three challenges like COVID-19 related disruptions in economies, Russian-Ukraine conflict and its adverse impact along with disruption in supply chain, mainly of food, fuel and fertilizer and the Central Banks across economies led by Federal Reserve responding with synchronised policy rate hikes to curb inflation, leading to appreciation of US Dollar and the widening of the Current Account Deficits (CAD) in net importing economies. The fourth challenge emerged as faced with the prospects of global stagflation, nations, feeling compelled to protect their respective economic space, thus slowing cross-border trade affecting overall growth. It adds that all along, the fifth challenge was festering as China experienced a considerable slowdown induced by its policies. The sixth medium-term challenge to growth was seen in the scarring from the pandemic brought in by the loss of education and income-earning opportunities.

The Survey notes that like the rest of the world, India, too, faced this extraordinary set of challenges but withstood them better than most economies.

In the last eleven months, the world economy has faced almost as many disruptions as caused by the pandemic in two years. The conflict caused the prices of critical commodities such as crude oil, natural gas, fertilisers, and wheat to soar. This strengthened the inflationary pressures that the global economic recovery had triggered, backed by massive fiscal stimuli and ultra-accommodative monetary policies undertaken to limit the output contraction in 2020. Inflation in Advanced Economies (AEs), which accounted for most of the global fiscal expansion and monetary easing, breached historical highs. Rising commodity prices also led to higher inflation in the Emerging Market Economies (EMEs), which otherwise were in the lower inflation zone by virtue of their governments undertaking a calibrated fiscal stimulus to address output contraction in 2020.

The Survey underlines that Inflation and monetary tightening led to a hardening of bond yields across economies and resulted in an outflow of equity capital from most of the economies around the world into the traditionally safe-haven market of the US. The capital flight subsequently led to the strengthening of the US Dollar against other currencies – the US Dollar index strengthened by 16.1 per cent between January and September 2022. The consequent depreciation of other currencies has been widening the CAD and increasing inflationary pressures in the net importing economies.